Despite the current inflation, the gold market has not moved and remains stable over the year. What if inflation was not the major financial factor moving gold?

Introduction

Inflation has become the most important search on google economics. From the Fed to the middle man, everybody is talking about inflation, and is constantly worrying about it.

Despite this environment, we could not understand why the gold market has not moved a bit. The precious metal is flat on the year, which, if we count inflation, means that gold lost a hell lot of value this year. We decided to go back in history in order to check that gold is really a hedge about inflation. By looking thoroughly at what happened in the past, we concluded that it is not exactly true, in the sense that inflation is not the primary financial factor which is moving gold.

In the first section of this article, we will study the impact of inflation on the gold price during major financial periods: the 70’s and the 2000’s.

In the second section of this article, we found a second financial factor which impacts much more the price of gold: the trade deficits. We will propose an indicator to anticipate large moves on gold prices based on inflation and trade deficits.

Impact of Inflation on the gold price from 70's to 2000's

1. How Does Inflation Impact Gold Prices?

More precise than inflation, we will study the real interest rates (real interest rate= inflation minus the risk-free rate paid by the Central Banks). This is fundamental because gold competes with the bond market (which is the biggest financial market of the world). If you have some cash, and you can earn an interest rate with it, by buying a bond, why would you hold gold? There is no reason for it. You’d rather hold the bond and earn the interest rate. But if the real interest is negative, and your bond position is losing money because inflation is higher than what your bond is paying you, then you would rather hold gold.

Let’s take two examples from History:

In 2022, the inflation rate in the US is 8%, the risk-free rate of the FED is 0%, and the 10-year US Treasury bond is 3% (this bond is a loan to the US government). If you think that inflation is going to be 8% or even more in the next coming years, why would you want to buy bonds and block your money to earn only 3% for the next 10 years. This does not make sense because the likelihood is negative. Even worst, if you just hold your cash, you make 0% interest, because the short-term interest rate is 0%. So, holding cash is a certain loss, and nobody would want to hold cash in those conditions. Therefore, buying gold makes perfectly sense, because you hold a commodity which will retain value throughout times of inflation.

In 1981, the inflation was 10%, but the short-term interest rate was 16%. Therefore, by holding cash you would directly make 6% with certainty. Contrary to what is happening today, cash was an interesting asset at that time. It was the most liquid asset, you could invest in any opportunity which would arise before you, and it was making 6% a year above inflation.

Real interest rate is the data that drives the behavior of investors towards cash. If the real interest rates are positive, or even flat, investors would use cash as a store of value, because it is the most liquid asset, and it is legal tender. But in periods of negative interest rate, as we are in today, investors lose a lot of money by holding cash (or bonds), and they are forced away to find another store of value for the times that they cannot find any good investment opportunities.

1a. The Crazy 1970s. Gold Price Raised by 2300%

In the chart below, we can see the price of gold and the real interest rates in the US throughout the 70’s. We can see the stable period of the 60’s. Gold was pegged to the dollar, and the real interest rates oscillated in a 2% range. In the early 70’s, following the oil shock of 1973, we can see that real interest rates collapsed into negative territory, due to raging inflation. The Fed was constantly behind the curve until 1980, and throughout the whole 70’s gold went up. We can clearly see a strong correlation between the price of gold and the real interest rate negative in the chart below. Gold rose when the rates were negative, and as soon as they became positive in 1980, gold had a severe correction and did not go up after that.

We need to stress out the amplitude of the moves here. In 1971, gold traded at US$35. By the end of that decade, gold touched US $850. That’s a 2300% gain in 10 years. Meanwhile, for stock investors in the west, the 70’s were pretty much a lost decade with a lot of volatility, and flat returns.

In the 1970s, the Fed printed more money to help control inflation (How can you ‘control’ inflation by printing more money? How can you do something so dumb and absurd?). Central banks also raised interest rates, but always behind the curve, meaning that inflation was constantly higher than interest rates. In 1971, the U.S. Fed funds rate was under 5 percent. In 1980, it was over 13 percent.

The 70’s are the archetype of buying gold to hedge against inflation. Yet, one can notice that the sharp move of gold arrived in the second part of the 70’s, quite late in the cycle.

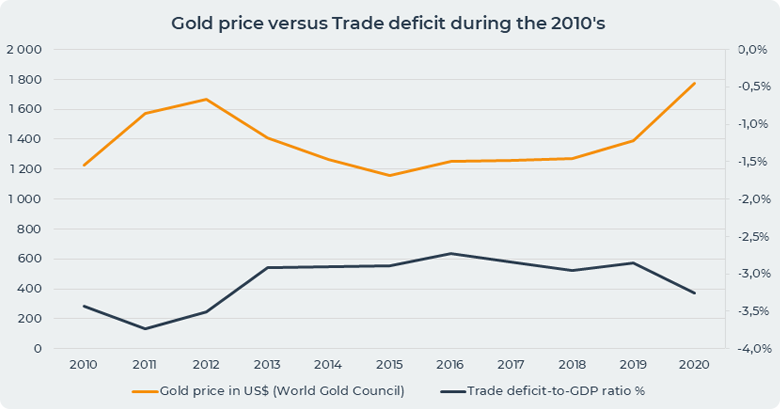

1b. A Second Period of Negative Interest Rates but With No Rise in the Price of Gold: The 2010’s

As we can see in the chart below, real interest rates were negative throughout the 2010’s. Yet the price of gold did not go up, it was more or less doing nothing whereas the price of the stock market was going to the roof.

Real rates were in average negative -2% in the first part of the decade. The Fed rate was around zero, and the inflation around 2%. Yet the price of gold did nothing like the 70’s.

This period invalidates the idea that gold is rising during periods of inflation. One could say that it was a mild inflation, and gold should rise only when there is a raging inflation of more than 5%. One could also say that the amount of gold mined every year is roughly 2% of the total amount of gold on the ground. So, the zero rate for gold is not 0% but -2%. But those explanations don’t hold when you look at the first part of the 70’s when inflation was raging, but gold took a lot of time to take off.

We looked for another explanation, and we found that trade deficit is much more relevant than inflation in order to explain rises of gold price.

Impact of the trade deficits on the gold price

2. Gold Correlated to Trade Deficit by 93% and Formation a Gold Bull Market.

Gold prices are only correlated at 61% to real interest rates. There is definitely an influence, but it does not systematically explain the moves of gold. As we have seen in the previous paragraph 1b, there are periods when real interest rates are negative, but gold does not rise.

On the other hand, the trade deficits combined to the negative interest rates are 93% correlated to gold prices and explain every bull run that the gold metal had.

Indeed, each time that the gold metal had a bull run, it happened simultaneously to a sharp increase of the trade deficit.

In the 70’s, as we can see in the chart below, gold prices started to take of not when the inflation aroused in 1973, but when the trade deficits began to drop sharply in 1977.

In the 2000’s, as we can see in the chart below, the price of gold started to take off in 2003, just when the trade deficit started to collapse sharply. We can see that in this period again the correlation of the events is astounding.

Finally, we can explain the mystery of the 2010’s when gold price did not go up whereas interest rates were negative (paragraph 1b above). During that period, trade deficits were steady, and so were gold prices. Although during the whole 2010’s interest rates were negative, gold did not move, and this is because trade deficits did not fall sharply. We can see in the chart below that trade deficits remain steady during that period.

2a. Negative Real Interest Rate and Sharp Decrease of Trade Deficit Equals a Gold Bull Market.

We then propose to build an indicator to identify the beginning of gold bull markets. We propose to take a mix of the real interest rates and the variation of the trade deficits. We show below the chart of this combined indicator.

The first time this combination happened was in the second part of the 70’s. At that time, there was a significant drop of the trade deficit compared to the previous decade and negative real interest rates. Trade deficits were only -1% for the US, but it was a new situation, as in the previous decade the US were constantly in trade surplus. They entered a trade deficit era at that time. The result of this combination of trade deficit gap plus real interest rates negative was a significant increase in the price of gold by 4 times from US$154 in 1974 to US$615 in the end of 1970s.

The second period of similar conditions happened in 2003-2005. In this period, the real interest rate was -1%, and the trade deficit plunged 2 times from -2% in 1998 to -5% in 2004. This caused another gold bull market in 2000s and the gold price increased from 279 $/Oz in 1999 to 700$/Oz by the end of 2007. This means a 250% increase.

The combined indicator identified in both cases the beginning of a bull market, where the price of gold was multiplied by 10.

Nowadays in 2022, we have similar conditions. The real interest rates are negative at -8% (since the inflation is at 8% and the Fed rate is at zero). And the trade deficit hit records low every year. Trump administration beat the infamous record of Obama’s administration. And Biden’s administration beat the infamous record of Trump’s administration. Whatever the president is, whatever the politics are, the US economy generates much wider trade deficit now than what they were doing in 2019. The combined signal indicates that we should be in the verge of a huge bull market in gold.

Conclusion

We have shown in the first part that inflation and negative interest rates don’t necessarily mean that gold will have huge rally. In the second half of the 70’s and in the 2000’s, it was the case because the US trade deficit has just widened consequently. But there are some other periods when there are negative interest rates and gold does not rally (for instance the 2010’s and the first half of the 70’s).

The signal requires both negative interest rates, and a recent drop in the trade deficit, to trigger almost certainly a rally in the gold market. It has worked in the past 60 years. If it is to work again, we should see very soon a huge rally for gold.

(Article written 25th June 2022; XAU= 1827; XAG= 21.2; XPT= 905; Oil= 111)