Solar’s rapid growth since 2023 is now a key driver of global energy transition and silver demand.

Record Solar Installations since 2023: What Changed, Who Led, and Why It Matters

Introduction

Since 2023, the global solar market has entered a new phase of expansion. What had already been a fast-growing sector became a record-breaking one. In 2023 alone, around 405–445 GW of new solar capacity was installed globally, a historical record.

Solar is now the main driver of new renewable power capacity worldwide. This shift is particularly important for the silver market, as photovoltaics are one of the key sources of industrial silver demand. Solar accounted for roughly 65% of renewable capacity growth in 2023.

The objective of this article is to explain where this growth came from, which countries led it, what type of investments supported it, and why 2023 became a turning point.

Which countries led the growth?

The expansion of solar capacity since 2023 has been dominated by China.

China alone accounted for the majority of global solar additions, installing significantly more capacity than any other country. China represented ~55–60% of global solar installations in 2023–2024. (International Energy Agency (IEA), Renewables 2024 Report)

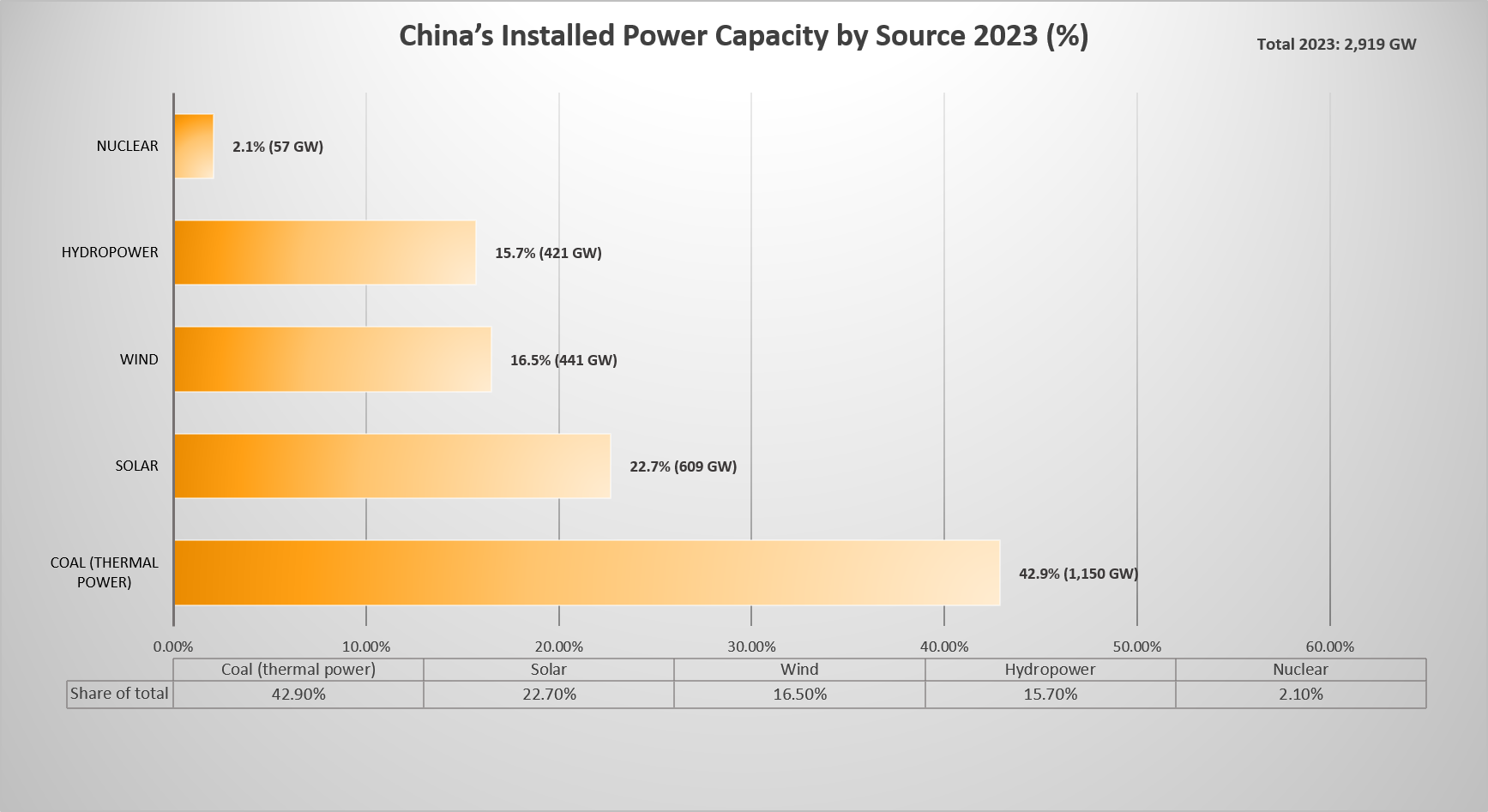

To quantify this dominance more precisely, it is useful to compare solar capacity with China’s broader power generation mix.

China’s energy mix: putting solar into perspective

To better understand the scale of solar expansion in China, it is essential to compare it with the country’s overall power generation capacity.

China’s installed power capacity is still dominated by coal, but renewable sources—particularly solar and wind—have grown rapidly and now represent a substantial share of the system.

This comparison highlights several important structural trends.

First, solar has already become one of the largest sources of installed capacity in China, exceeding hydroelectric power and approaching wind levels. With roughly 600–700 GW installed, solar represents over 20% of the country’s total capacity.

Second, while coal remains the dominant energy source, solar capacity has reached more than half of coal’s installed base. This is a significant shift, considering that solar capacity was marginal just a decade ago.

Third, when combined, renewable sources—solar, wind, and hydro— represent more than half of China’s installed capacity. This reflects a structural transition in the energy system, even if coal continues to dominate actual electricity generation due to its higher load factor.

Overall, the data confirms that solar is no longer a marginal or emerging technology in China. It has become a key pillar of the country’s power infrastructure and a key driver of global energy transition dynamics.

Outside China, the main contributors were the European Union, the United States, India, and Brazil. Together, China, the US, India, Germany, and Brazil accounted for ~75% of global solar additions in 2024.

The European Union saw strong growth driven by Germany and Southern Europe. The United States experienced a rebound after a slower 2022. India and Brazil also showed consistent expansion.

In summary, the global solar boom is highly concentrated, with China as the primary driver and a second group of large economies supporting the trend.

What industry drove the expansion?

Solar growth has been driven primarily by the power generation sector, especially utility-scale projects.

Large solar farms represent the majority of new capacity, as they benefit from economies of scale and long-term contracts.

Utility-scale solar represented more than 60–70% of new installations globally in recent years. (Ember, Global Electricity Review 2024)

However, distributed solar also played an important role. In 2024, around 180-200GW of new capacity came from rooftop and distributed systems. Commercial and industrial systems expanded as companies sought lower electricity costs, while residential adoption increased in regions with supportive policies and high energy prices.

This combination of utility-scale and distributed installations explains the strength and resilience of the market.

Private vs government investment

The expansion of solar energy is largely financed by private capital. Developers, utilities, corporations, and households are responsible for the majority of investments in solar installations. Global solar investment exceeded USD 480 billion in 2023 alone. (IEA, 2024)

Programs such as tax incentives, subsidies, auctions, and energy transition strategies have been essential in accelerating deployment.

The most accurate interpretation is that solar growth is driven by private investment, but enabled and guided by public policy.

Why 2023 became the turning point

The solar market was already growing before 2023, but several factors aligned to create a breakout year.

First, solar panel prices declined significantly, making projects more economically attractive. Module prices dropped by more than 45% between early 2023 and 2024 due to oversupply.

Second, major policy frameworks introduced in previous years began to translate into real installations.

Third, the global energy crisis increased the need for energy security, pushing governments and businesses toward solar solutions.

Fourth, manufacturing capacity expanded rapidly, removing previous supply constraints. Global solar manufacturing capacity exceeded 1,100 GW by 2024, far above demand.

These combined effects explain why 2023 marked a clear acceleration rather than a gradual continuation of previous trends.

Future outlook

The outlook for solar remains strong.

Global capacity is expected to continue growing rapidly over the coming years, supported by long-term decarbonization targets and electrification trends.

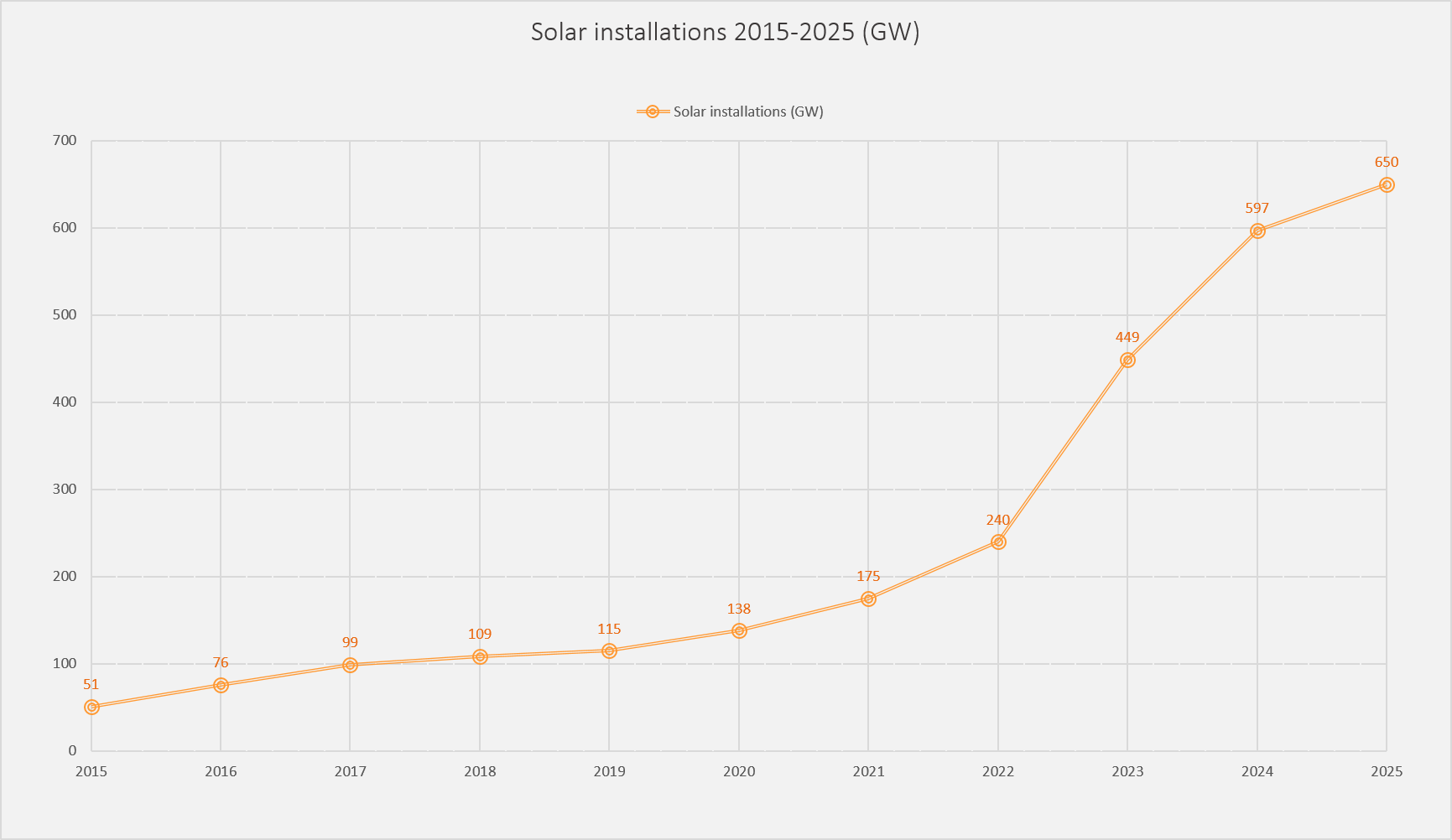

Around 550–600 GW of solar capacity was added in 2024 alone, a new all-time record. Total global solar capacity exceeded ~2.2 TW by 2024.

Preliminary estimates and industry forecasts suggest that global solar installations in 2025 could reach approximately 600–700 GW, continuing the acceleration observed since 2023. (International Energy Agency (IEA), Renewables 2024 Report, SolarPower Europe)

However, new challenges are emerging, including grid constraints, permitting delays, and the need for energy storage.

Despite these challenges, solar is expected to remain the dominant source of new renewable capacity worldwide.

Implications for silver

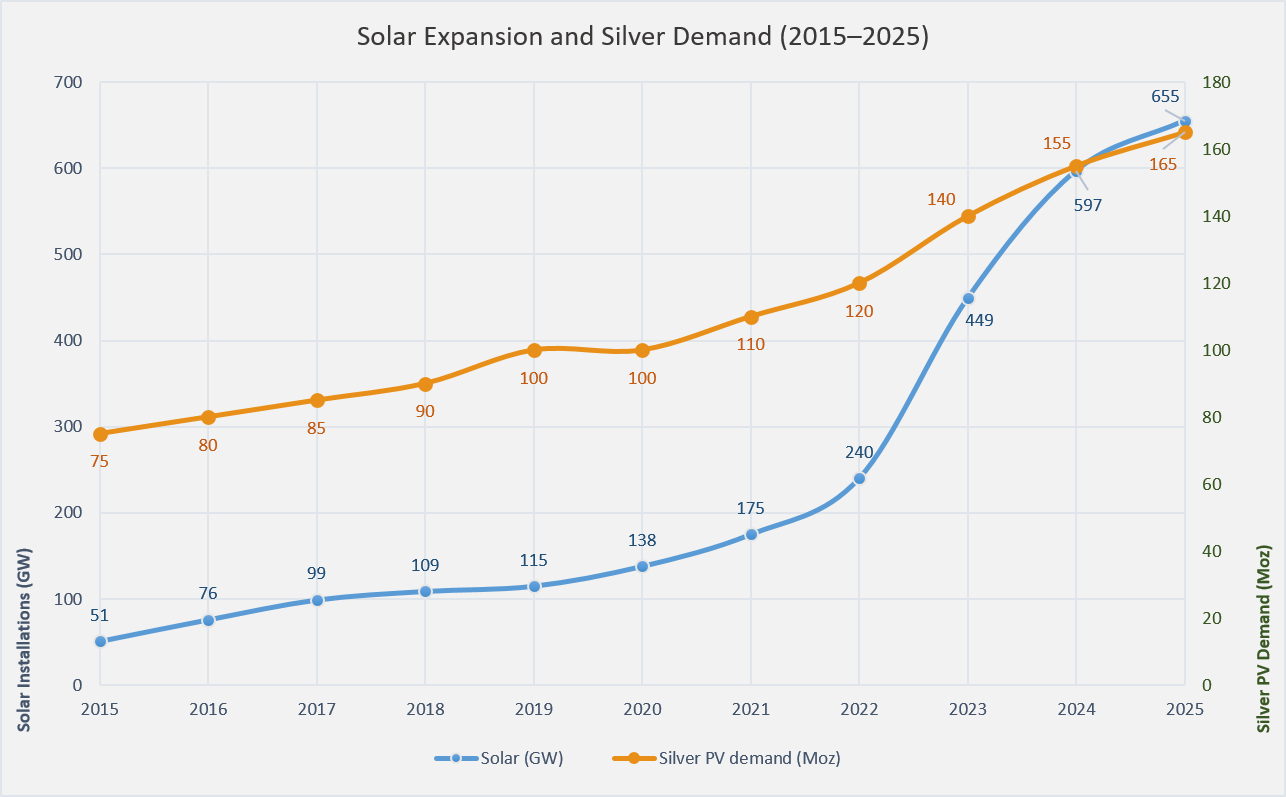

For the silver market, the rise of solar energy has become a structural driver of demand, rather than a cyclical one.

Silver remains an essential component in photovoltaic (PV) cells due to its unmatched electrical conductivity, enabling efficient energy transfer within solar panels. Although technological improvements have gradually reduced the amount of silver required per panel, this reduction has been outweighed by the rapid and sustained expansion of global solar installations.

As a result, total silver demand from the photovoltaic sector continues to increase in absolute terms. Recent industry estimates suggest that PV applications now account for approximately 12–15% of global silver demand, equivalent to around 140–160 million ounces per year.

In this context, the continued growth of solar capacity is not only a key feature of the energy transition, but also a fundamental support for long-term silver demand.

Despite rapid growth in solar installations, silver demand increases at a slower pace due to ongoing reductions in silver usage per panel.

Conclusion

Since 2023, solar energy has entered a new phase of rapid expansion. China has led the growth, supported by major economies such as the European Union, the United States, India, and Brazil.

Annual installations increased from ~400 GW (2023) to ~550–600 GW (2024), confirming an acceleration phase rather than linear growth.

The expansion has been driven by a combination of private investment and strong government policy support.

The turning point in 2023 was the result of falling costs, policy momentum, energy security concerns, and expanded manufacturing capacity.

Looking forward, solar is expected to remain a central pillar of the global energy transition, with significant implications for industrial demand, including silver.